Complete Guide

Student Loan Repayment Guide: How to Manage and Pay Back Your Loans

- ~15 min read

- Written by CFPs & AFCs

- Backed by national research

You graduated. You landed the job. And now there is a number on a screen that you are not totally sure how to deal with.

Student loan repayment is one of those things nobody really teaches you. You signed documents years ago, and now those documents want something back. If you are feeling behind or confused, that is completely normal.

According to the Federal Reserve, nearly 43% of adults who attended college have taken on student debt, and a significant portion of borrowers in their 20s and 30s report feeling stressed about their finances. You are not the only one figuring this out.

This guide is written specifically for borrowers whose loans were first disbursed before July 1, 2026, and who do not plan to take out new federal loans on or after that date. That matters right now, because major changes to the federal loan system are underway, and which rules apply to you depends on when your loans were made.

This guide walks you through the whole picture, step by step, without jargon. By the end, you will know exactly where to start.

A note about this guide and who wrote it

RedSky Money is a nonprofit organization built specifically to give early-career adults access to professional financial coaching at no cost. Our coaches are Certified Financial Planners (CFPs) and Accredited Financial Counselors (AFCs). We do not sell financial products. We do not offer investment services. We do not upsell you into anything. Coaching is always free, because that is the entire point of why we exist.

We wrote this guide because people starting out have real questions and nowhere to go for honest answers. If anything here raises a question specific to your situation, you can book a free Discovery Call with one of our coaches at redskymoney.org. No pitch. No catch.

In This Guide:

- First Steps: How to Find Your Student Loan Details

- The Post-Graduation Timeline: When Do Your Payments Start?

- Choosing the Best Federal Repayment Plan

- What to Do If You Can’t Afford Your Monthly Payment

- Forgiveness and Assistance: Getting Help with Your Debt

- Strategies to Pay Off Your Loans Faster

- Refinancing Student Loans: Is It Right for You?

- Talk to a Coach: Free One-on-One Support

- You Are More Prepared Than You Think

- Frequently Asked Questions

- Sources

STEP 1

How to Find Your Student Loan Details

Before you can make a plan, you need the facts. A lot of people skip this step because it feels intimidating. But the information is out there, and once you have it, the whole picture gets a lot clearer.

Identifying Your Student Loan Servicer

Your loan servicer is the company that actually manages your loan account. They collect your payments, help you enroll in plans, and handle any questions about your balance. If you have federal loans, your servicer was assigned to you, so you might not even know who they are.

Here is how to find out:

- Go to StudentAid.gov and log in with your FSA ID

- Your servicer information will be listed on your account dashboard

- If you have multiple loans, you may have more than one servicer

Private loans work differently. Check your old emails from when you were in school, or log in to your school’s financial aid portal. Your lender will be named there.

Finding Your Total Balance and Interest Rates on StudentAid.gov

Once you are logged into StudentAid.gov, look for the “Loan Details” section. This will show you:

- Your total balance for each loan

- The interest rate attached to each one

- Whether the loan is subsidized or unsubsidized

Write these numbers down or screenshot them. Knowing your exact balance and interest rates is the foundation of any good repayment plan.

Why this matters

Unsubsidized loans accrue interest even during school and your grace period. If your balance looks higher than what you originally borrowed, that is why. The sooner you understand your specific loan types, the better positioned you are to make smart decisions.

Federal vs. Private Loans: Why the Difference Matters

This is one of the most important distinctions in the student loan world. Federal loans come with income-driven repayment options, forgiveness programs, and hardship protections. Private loans generally do not.

Federal Loans

Multiple repayment plan options

Income-driven repayment available

Potential forgiveness programs

Deferment and forbearance options

6-month grace period after graduation (typical)

Private Loans

Fixed or variable rates set by the lender

No income-driven repayment

No federal forgiveness programs

Limited hardship options

Terms vary by lender

Knowing which type of loans you have changes everything about how you approach repayment. If you are not sure, StudentAid.gov is the place to check.

Figuring out your loans can feel like untangling a knot. If you want help making sense of your numbers, you can schedule a free one-on-one conversation with a RedSky Money coach.

STEP 2

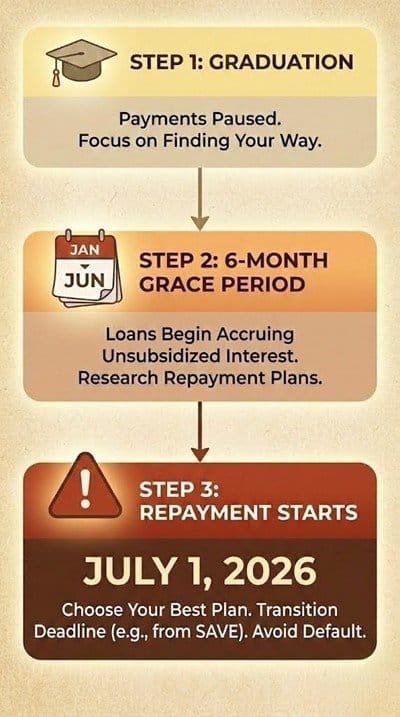

The Post-Graduation Timeline: When Do Your Payments Start?

One of the biggest surprises for recent graduates is how fast the clock moves after walking off the stage.

How the 6-Month Grace Period Works

For most federal student loans, you have a 6-month grace period after graduation, leaving school, or dropping below half-time enrollment. During this window, payments are not required.

But here is what a lot of people miss: interest is still building on unsubsidized loans during this period. If you can make small payments during the grace period, you will save money in the long run.

Setting Up Your FSA ID and Loan Portal Access

Your FSA ID is your username and password for the federal student aid system. If you have not set one up yet, start there. Go to StudentAid.gov and create your account using your Social Security number and personal information.

Once you are in, you can see your loan details, enroll in repayment plans, and communicate with your servicer. Some people also need to log in separately to their servicer’s website for direct payment management. Your servicer should have sent you login instructions around graduation.

Critical Deadlines for Recent Graduates

Here is a quick list of things to get on your radar in your first year after graduation:

- 6 months after graduation: federal loan payments begin

- Before first payment: review your repayment plan options and enroll in the one that fits your income

- Within 90 days of starting a new job: ask your employer about student loan assistance benefits

- Annually: recertify your income if you are on an income-driven repayment plan

Not sure what your timeline looks like or which steps come next for you specifically? A free Discovery Call can help you map it out.

STEP 3

Choosing the Best Federal Repayment Plan

Federal student loan repayment changed significantly in 2025 and 2026. If your loans were first disbursed before July 1, 2026, you have more choices than new borrowers, but the landscape has shifted. Here is what is available to you right now.

The SAVE Plan has ended

The Saving on a Valuable Education (SAVE) plan, a Biden-era income-driven repayment option, was permanently terminated in March 2026 following a court settlement. If you were enrolled in SAVE or its forbearance, you need to choose a new repayment plan. Contact your servicer or visit StudentAid.gov to switch. Borrowers who do not switch by the deadline communicated by their servicer will be automatically moved to the Standard Repayment Plan or the new Tiered Standard Plan.

The Plans Still Available to You (Pre-July 2026 Borrowers)

Because all of your loans were first disbursed before July 1, 2026, you retain access to the following repayment plans, subject to eligibility:

- Standard Repayment Plan

- Graduated Repayment Plan

- Extended Repayment Plan

- Income-Based Repayment (IBR) Plan

- Income-Contingent Repayment (ICR) Plan

- Pay As You Earn (PAYE) Plan

- Repayment Assistance Plan (RAP) — launching July 1, 2026

The one plan you will not have access to is the new Tiered Standard Plan, which is designed for borrowers with loans first disbursed on or after July 1, 2026.

You can switch between any of the plans for which you are eligible at any time.

Important: Two plans are being retired

PAYE and ICR will be retired no later than July 1, 2028. If you are currently on PAYE or ICR, the Department of Education is working on a transition plan. Most borrowers will be moved to IBR or RAP. You do not need to take action right now, but it is good to know so you can plan ahead.

Standard, Graduated, and Extended Repayment Plans

These are the fixed-payment options. No income verification required, and no annual recertification.

Standard Repayment spreads your loans over 10 years with equal monthly payments. It is the default plan. If you can afford the payments, it is often the fastest way to pay off debt and the least you will pay in total interest.

Graduated Repayment starts with lower payments that increase every two years. It is designed for borrowers who expect their income to grow. The total repayment period is still 10 years, but you pay more in interest overall because early payments are smaller.

Extended Repayment stretches payments out to up to 25 years. To qualify, you need at least $30,000 in outstanding federal loans. Payments can be fixed or graduated. Your monthly payment is lower, but you will pay significantly more in total interest over the life of the loan.

Income-Based Repayment (IBR)

IBR is one of the most important options available right now, especially with SAVE gone. It caps your monthly payment based on your income and family size, and forgives any remaining balance after 20 or 25 years.

Which version you get depends on when you first borrowed:

- Borrowed before July 1, 2014: payments are 15% of discretionary income, forgiveness after 25 years

- Borrowed on or after July 1, 2014: payments are 10% of discretionary income, forgiveness after 20 years

Your monthly payment under IBR will never exceed what you would pay under the Standard 10-year plan, even if your income rises.

IBR eligibility just got broader

As of July 4, 2025, the partial financial hardship requirement was removed from IBR. Previously, you could only enroll if your IBR payment would be lower than your Standard 10-year payment. That rule no longer exists. Any borrower with eligible loans can now enroll in IBR regardless of income. If you were denied IBR in the past for this reason, you can reapply.

IBR is also one of two IDR plans that will remain permanently available after July 2028. The Department of Education recommends it as a reliable bridge plan for borrowers currently on SAVE who need to switch now.

PAYE and ICR: Still Available, But Sunsetting in 2028

Pay As You Earn (PAYE) caps payments at 10% of discretionary income and forgives balances after 20 years. It requires that you meet certain loan origination date requirements, and still requires a partial financial hardship to enroll. Note: the partial financial hardship requirement was removed for IBR by the One Big Beautiful Bill Act, but that change did not extend to PAYE. PAYE still requires it.

Income-Contingent Repayment (ICR) calculates your payment as either 20% of discretionary income or what you would pay on a 12-year fixed plan, whichever is lower. Forgiveness comes after 25 years. ICR is notable because it is the only income-driven plan that has been available to consolidated Parent PLUS loan borrowers, but that window is closing.

If you have Parent PLUS loans: act before July 1, 2026

ICR is currently the only income-driven repayment option for Parent PLUS loan borrowers who consolidate into a Direct Consolidation Loan. If you consolidate before July 1, 2026, you can still access ICR. If you consolidate after that date, Parent PLUS borrowers lose access to income-driven repayment entirely, since Parent PLUS loans are not eligible for IBR or RAP.

Both PAYE and ICR will be retired no later than July 1, 2028. Borrowers on those plans will need to transition to IBR or RAP before that date.

The Repayment Assistance Plan (RAP): The New Income-Driven Option

RAP is a brand-new income-driven repayment plan created by the One Big Beautiful Bill Act, signed July 4, 2025. It launches July 1, 2026 and will be available to you as a pre-July 2026 borrower.

Unlike existing IDR plans, RAP bases your payment on a percentage of your total adjusted gross income (AGI) rather than your discretionary income. Payments run from 1% to 10% of AGI depending on your income bracket, with a minimum monthly payment of $10. If you have dependents, $50 per dependent is subtracted from your monthly payment.

Here is how the payment tiers look:

Annual Income

$0 to $10,000

$10,001 to $20,000

$20,001 to $30,000

$30,001 to $40,000

$40,001 to $55,000

$55,001 to $70,000

$70,001 to $85,000

$85,001 to $100,000

Over $100,000

RAP Payment Rate

$10 per month (flat minimum)

1% of AGI

2% of AGI

3% of AGI

4% of AGI

5% of AGI

6% of AGI

8% of AGI

10% of AGI

Example: A single borrower earning $55,000 per year with no dependents would pay roughly $229 per month under RAP ($55,000 x 5% / 12).

RAP forgives any remaining balance after 360 qualifying payments, which is 30 years. That is a longer forgiveness timeline than IBR’s 20-year path for most recent graduates. RAP also waives any unpaid interest when you make a full, on-time payment, which prevents your balance from growing even when your payment is small.

A note on taxes and forgiven balances

The federal tax exemption for forgiven student loan balances expired on December 31, 2025. Under current law, any balance forgiven through IDR plans (IBR, RAP, PAYE, or ICR) after that date is treated as taxable income in the year it is forgiven. PSLF forgiveness remains tax-free. This does not affect your day-to-day repayment, but it is worth knowing if you are planning around a forgiveness date years from now.

RAP and PSLF

If you are working toward Public Service Loan Forgiveness, payments made under RAP count toward the 120-payment PSLF requirement, the same as any qualifying IDR plan.

One important note: RAP does not cap your payment the way IBR does. If your income rises significantly, your payment rises too. IBR caps at the Standard 10-year payment amount; RAP does not have that ceiling.

Which Plan Is Right for You?

Here is a simplified way to think about it:

Plan

Standard Repayment

Graduated Repayment

Extended Repayment

Income-Based Repayment (IBR)

Income-Contingent Repayment

Pay As You Earn (PAYE)

Repayment Assistance Plan (RAP)

Payment Amount

Fixed; based on balance

Starts low, increases every 2 years

Fixed or graduated

10% or 15% of discretionary income*

20% of discretionary income or 12-year fixed, whichever is lower

1% to 10% of total AGI (tiered by income)

1% to 10% of total AGI (tiered by income)

Forgiveness Timeline

10 years (no forgiveness needed)

10 years (no forgiveness needed)

Up to 25 years

20 or 25 years*

25 years

20 years

30 years

Best For

Borrowers who can afford standard payments and want to pay off quickly

Borrowers expecting income growth

Borrowers with $30,000+ in loans needing lower payments

Most borrowers wanting income-based payments with a long-term forgiveness path

Sunsetting July 2028; best alternative for Parent PLUS (if consolidated before July 2026)

Sunsetting July 2028; available to borrowers who first borrowed after Oct. 1, 2007

Borrowers who want to preserve income-based payments after PAYE/ICR sunset in 2028

* IBR payment rate (10% or 15%) and forgiveness timeline (20 or 25 years) depend on when you first borrowed. Borrowers who first borrowed on or after July 1, 2014 get the more favorable 10% rate and 20-year forgiveness term.

The Loan Simulator at StudentAid.gov is a useful free tool for comparing how your monthly payment would look under each plan based on your actual loan balance and income.

Repayment options right now are more complicated than they have been in years. If you want a second set of eyes on your specific situation, a RedSky coach can walk through your options with you at no cost.

STEP 4

What to Do If You Can't Afford Your Monthly Payment

Life does not always go according to plan. If your payment feels too high right now, you have options. Ignoring the problem is the one thing you should not do.

Research by the Consumer Financial Protection Bureau found that many borrowers who default on student loans did not know relief options were available. Missing payments has real consequences, but there are legitimate ways to pause or reduce them.

Deferment vs. Forbearance: Temporary Relief

Both deferment and forbearance let you temporarily stop or reduce payments. The difference is mostly about interest.

Deferment

Interest may not accrue on subsidized loans

Requires qualifying circumstances (unemployment, school, etc.)

May count toward forgiveness timelines depending on plan

Forbearance

Interest accrues on all loan types

Generally easier to get approved

May pause forgiveness count depending on plan

Neither option should be your long-term plan. They are tools for a short stretch of difficulty.

Applying for a Lower Payment Based on Income

If your income has changed or is simply low relative to your loan balance, you can apply for income-driven repayment at StudentAid.gov. You will need to provide income information, and your payment will be recalculated based on your actual earnings.

Some borrowers with high loan balances and entry-level salaries qualify for very low monthly payments. Under RAP, borrowers earning $10,000 per year or less pay just $10 per month.

Avoiding Default and Delinquency

Missing a payment by 90 days puts your loan in delinquency. After 270 days, federal loans go into default. Default can damage your credit score significantly, trigger wage garnishment, and disqualify you from future federal aid.

If you are approaching a payment you cannot make, contact your servicer before it happens. They have options available, and acting early protects you.

If you are worried about an upcoming payment or already feeling behind, a coach can help you figure out your next move. There is no judgment, just options.

STEP 5

Forgiveness and Assistance: Getting Help with Your Debt

Some borrowers will qualify for programs that reduce or eliminate their remaining balance after a period of qualifying payments. These programs are real, but they have specific requirements that matter.

Public Service Loan Forgiveness (PSLF) Requirements

PSLF forgives the remaining balance on your federal loans after you make 120 qualifying payments while working full-time for a qualifying employer. Qualifying employers include government agencies and most nonprofit organizations.

Important things to know:

- You must be on a qualifying income-driven repayment plan (or, starting July 2026, on the RAP plan)

- Payments must be on time and in full

- Employment must be certified with your servicer

- The 120 payments do not need to be consecutive

PSLF rule changes effective July 1, 2026

Final regulations published in October 2025 allow the Department of Education to deny PSLF forgiveness to workers at employers found to have a ‘substantial illegal purpose,’ with that determination left to the Education Secretary. Legal challenges are ongoing. If you are pursuing PSLF, continue submitting your Employment Certification Form annually and monitor StudentAid.gov for updates.

PSLF documentation matters. Submit your Employment Certification Form every year, not just at the end of your 10-year period.

Career-Specific Forgiveness (Teachers, Nurses, etc.)

There are additional forgiveness programs beyond PSLF for certain career fields:

- Teacher Loan Forgiveness: Up to $17,500 for teachers in low-income schools after 5 years of service

- Nurse Corps Loan Repayment: For registered nurses working in critical shortage facilities

- State-level programs: Many states offer loan repayment assistance for healthcare, legal aid, and other fields

Eligibility rules vary. Always verify current program terms through official government or employer sources.

Asking Your Employer about Repayment Benefits

This one is underused. Since 2020, employers have been able to contribute up to $5,250 per year tax-free toward an employee’s student loan debt under Section 127 of the tax code. Not every company offers this benefit, but it is worth asking your HR department directly.

Forgiveness programs have a lot of fine print. If you want to know whether PSLF or another program could apply to your situation, bring your questions to a free Discovery Call.

STEP 6

Strategies to Pay Off Your Loans Faster

If you have room in your budget and want to get out from under this debt sooner, there are a few strategies worth knowing about.

The Debt Snowball vs. Debt Avalanche Methods

Both are popular approaches for paying off multiple loans. They just prioritize differently.

Debt Snowball

Pay off the smallest balance first

Good for motivation and momentum

You see early wins quickly

Debt Avalanche

Pay off the highest interest rate first

Saves the most money in interest over time

May take longer before a loan disappears

There is no wrong answer here. If seeing progress quickly keeps you on track, the snowball works well. If minimizing total interest paid is your priority, the avalanche wins on paper.

For more practical budgeting ideas that free up cash for loan payments, see our blog post on 5 Simple Budgeting Hacks That Actually Work.

The Power of Principal-Only Extra Payments

Even a small extra payment each month, when applied to principal rather than future interest, can shorten your repayment timeline noticeably. Make sure you designate any extra payment as applying to principal. Contact your servicer to confirm how to do this, since not all servicers apply extra payments the same way by default.

Reducing Your Interest Rate with Auto-Pay

Most federal loan servicers offer a 0.25% interest rate reduction when you enroll in automatic payments. It is a small number, but over years of repayment it adds up. It also protects you from missing a payment accidentally.

If you want to build a real payoff timeline around your income and expenses, a RedSky coach can help you put together a cash flow plan that accounts for your loans.

STEP 7

Refinancing Student Loans: Is It Right for You?

Refinancing means taking out a new private loan to pay off your existing loans, ideally at a lower interest rate. It can make sense in some situations, but it comes with a trade-off that is important to understand before moving forward.

The Risks of Refinancing Federal Loans into Private Loans

Read this before refinancing federal loans

When you refinance federal loans into a private loan, you permanently lose access to federal protections. That includes income-driven repayment, forgiveness programs, deferment, forbearance, and PSLF eligibility. This decision cannot be undone.

If there is any chance you might need those federal protections, refinancing is likely not the right call. This includes anyone working toward PSLF, anyone in an income-sensitive job, or anyone whose income may be unpredictable.

When Private Refinancing Makes Financial Sense

Private refinancing may be worth exploring if:

- You have only private loans to begin with (no federal loans at stake)

- You have a strong credit score and stable, higher income

- You can qualify for a significantly lower interest rate

- You are confident you will not need income-driven repayment or forgiveness

Even then, compare offers carefully. Look at the total amount paid over the life of the loan, not just the monthly payment.

Not sure if refinancing is a good move for your specific situation? A RedSky Money coach can walk through your loan types, income, and goals with you before you make a decision.

STEP 8

Talk to a Coach: Free One-on-One Support

Student loan repayment is not one-size-fits-all. The right plan depends on your income, your loan types, your career goals, and what you can realistically afford each month.

RedSky Money offers free financial coaching for early-career adults who are trying to get a handle on their finances. A Discovery Call is a no-commitment conversation where you can share where you are and get real, practical guidance on your next steps.

You do not need to have everything figured out before you reach out. That is what the call is for.

What to expect from a free Discovery Call

A 15-20 minute conversation with a RedSky Money coach

No sales pressure. No product pitches.

Initial consultation designed to determine if there is a mutual fit for a working relationship

You discuss your current financial struggles, goals, and needs, while the coach explains how they can assist you.

STEP 9

You Are More Prepared Than You Think

Student loans can feel overwhelming, but the path forward is manageable when you break it into steps. Find your servicer. Know your loan types. Understand your repayment options. And do not go it alone if you do not have to.

The financial decisions you make in your 20s and 30s have long-term effects, but small, smart moves made now can make a real difference over time.

You have got this. And if you want company for the journey, RedSky Money is here.

FAQs

Frequently Asked Questions

What if I do not remember who my student loan servicer is?

Start at StudentAid.gov. Log in with your FSA ID and your servicer information will appear on your account dashboard. If you have private loans, check old emails from your lender or contact your school's financial aid office.

The SAVE plan is gone. What should I do right now?

If you were enrolled in SAVE or have been in SAVE-related forbearance, you need to choose a new repayment plan. The Department of Education is contacting affected borrowers and giving them 90 days to switch after being notified. If you do not choose a plan within that window, you will be automatically moved to the Standard Repayment Plan or the Tiered Standard Plan. For most borrowers, IBR is the most recommended alternative right now. Visit StudentAid.gov or contact your servicer to apply.

Can I switch repayment plans if my income changes?

Yes. You can switch between federal repayment plans at any time. If your income drops, switching to an income-driven plan can lower your monthly payment significantly. Contact your servicer or apply at StudentAid.gov.

Is it possible to qualify for $0 per month in payments?

Possibly, depending on your income and the plan you are on. Under IBR, borrowers whose income is at or below 150% of the federal poverty guideline may qualify for a $0 monthly payment. Under RAP, the minimum is $10 per month for those earning $10,000 or less annually. You still need to be enrolled in the plan and recertify your income each year.

How do I know if my job qualifies for Public Service Loan Forgiveness?

Use the PSLF Help Tool on StudentAid.gov to check your employer's eligibility. Government agencies at any level and most nonprofit organizations typically qualify. Private companies generally do not. When in doubt, submit your Employment Certification Form to get an official answer from your servicer. Keep in mind that new PSLF regulations take effect July 1, 2026, and eligibility rules for certain employers may be reviewed under those regulations.

Sources

- Federal Reserve Board, 2023 Report on the Economic Well-Being of U.S. Households (SHED)

- U.S. Department of Education, One Big Beautiful Bill Act: Summary of Federal Student Loan Provisions, July 2025

- U.S. Department of Education press release, March 27, 2026: Announces Next Steps for Borrowers Enrolled in the Unlawful SAVE Plan

- StudentAid.gov, Announcements and Events: Big Updates for Student Loan Borrowers, 2026

- Consumer Financial Protection Bureau (CFPB), Student Loan Repayment and Borrower Outcomes Reports

- FINRA Investor Education Foundation, 2022 National Financial Capability Study

- Pew Research Center, Student Loan Debt in America Reports

- Internal Revenue Service (IRS), Publication on Educational Assistance Programs (Section 127)

- U.S. Department of Education, PSLF Final Regulations, October 2025 (effective July 1, 2026)

- MOHELA Federal Student Aid, IDR Plans and Repayment Options, updated March 2026